Anthony Albanese and Peter Dutton have announced major changes they say will help first time buyers. Economists fear the Coalition’s tax breaks could end up costing billions of dollars more.

- Originally Published on Financial Review

- April 5–6, 2025

- By Tom Dusevic

Housing affordability has long been a priority issue for voters at federal elections, but as the “great Australian dream” of homeownership slips out of reach, both sides have amplified their property policies.

On Sunday, Prime Minister Anthony Albanese and Opposition Leader Peter Dutton announced new interventions in the housing market, and each claimed to be doing more to help first home buyers.

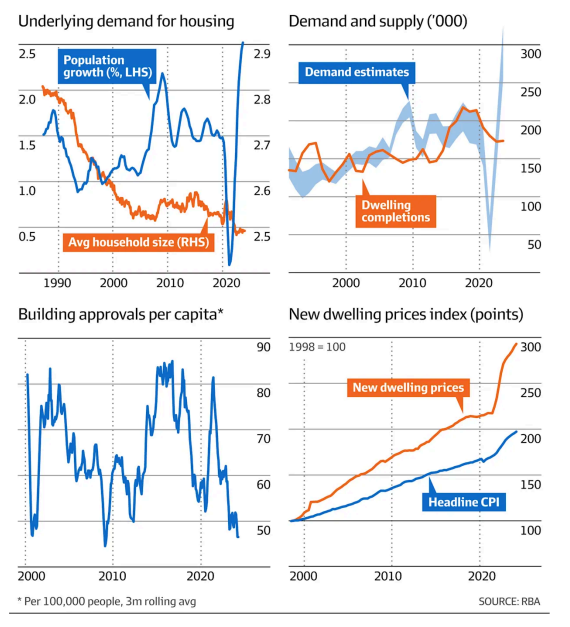

Most economists are cynical about the measures, saying these will simply increase demand for housing in a market where the supply of new homes is constrained because of government regulation and the high cost of construction.

The expected result? Higher house prices and more risky debt levels.

Nonetheless, there are differences between the Labor and Coalition housing policies that will have varying consequences for different buyers and sectors of the property market.

In the most radical move, Dutton is pledging to introduce tax deductions on mortgage interest for first home buyers

Interest paid on the first $650,000 of a mortgage would be eligible for a tax deduction against income for up to five years, saving an average buyer about $12,000 a year or $60,000 in total.

Albanese unveiled a $10 billion investment to build 100,000 new homes exclusively for first home buyers.

Labor also pledged to expand the former Morrison government’s first home guarantee from 35,000 first-time buyers to an unlimited number of people. This provides free government-backed lenders’ mortgage insurance to buyers with deposits as little as 5 per cent, helping them get

into the market without the need for the 20 per cent deposit they would require if a bank was willing to lend to them.

Both parties had previously announced other measures, such as the Coalition enabling first buyers to access $50,000 of their superannuation

funds and Labor’s $10 billion Housing Australia Future Fund for social and affordable housing.

Here’s what the new policies mean for different parts of the market.

What buyers and properties are eligible?

Under the Coalition, mortgage interest deductions will be available to individuals earning up to $175,000 and joint applicants with combined incomes of up to $250,000.

There is no cap on the overall mortgage size or home price, but only the interest on the first $650,000 of the loan will qualify for deductions.

Labor’s expanded mortgage insurance guarantee will become available for all first purchases worth up to $1.5 million in Sydney, $950,000 in Melbourne, $1 million in Brisbane and Canberra, $850,000 in Perth, $900,000 in Adelaide, and $700,000 in Hobart.

The existing guarantee scheme is restricte…….

Download the PDF to read full blog: